By Julian Zegelman

Having spent the last few years investing in and advising Seed and Series A stage startups, I grew suspicious of the prolonged bull run and expected a correction in the private and public markets. However, I could have never imagined that the correction will manifest itself as a world wide pandemic, causing a shut down of commercial activity, and prospects of recession of an unprecedented magnitude. The purpose of this article is to share my personal opinions on what the venture capital markets might look like in the next six to twelve months. Since I largely invest and work with Seed and Series A companies, I will focus on these cases below:

A. Tales of Crises Past

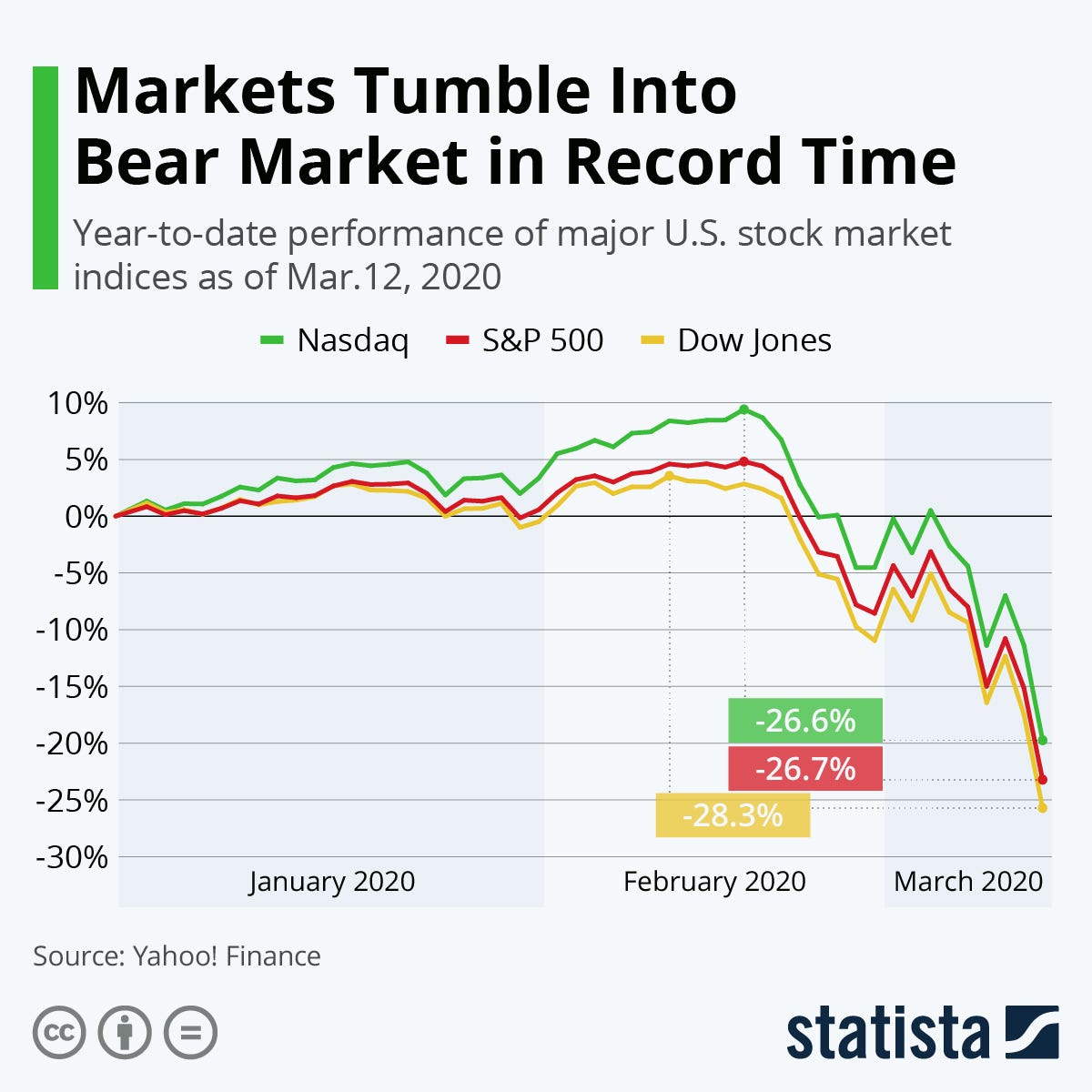

As a former VC-backed entrepreneur turned active angel investor and tech investment banker at Jaguar Capital Advisors (www.jaguarcapital.io), I am no stranger to crisis. My very first startup GetHoused was the love child of a few starry eyed sophomores at University of California San Diego back in the late 1990s. When the dot com bust hit in 2000, NASDAQ lost 25% over one fateful April week and we watched a startup fairyland disappear almost overnight. The company, a real estate search engine, never quite recovered from that one.

My second startup, Rolith, Inc., a deep tech with roots at Stanford, was started in the midst of the financial meltdown in 2008. We held on to our rails and weathered two very stormy years before things turned for the better. That company raised a few venture rounds and was successfully sold to a strategic buyer in 2016.

Having spend the last few years investing in and advising Seed and Series A stage startups, I grew suspicious of the prolonged bull run and expected a correction in the private and public markets. However, I could have never imagined that the correction will manifest itself as a world wide pandemic, causing a shut down of commercial activity, and prospects of recession of an unprecedented magnitude. The purpose of this article is to share my personal opinions on what the venture capital markets might look like in the next six to twelve months. Since I largely invest and work with Seed and Series A companies, I will focus on these cases below.

B. Current Situation

From my vantage point, currently Seed and Series A investors in the US are falling into one of the following three categories:

(a) Putting a temporary freeze on any deals, i.e. not investing. Most will still honor an existing term sheet, however, I am seeing and hearing an alarming number of renegotiations and/or cancelled term sheets out there. If the public markets continue to deteriorate, it is likely to trigger a corresponding growth in number of angels and/or VCs who are holding on to their cash.

(b) Only investing in existing portfolio companies, i.e. bridges, round extensions, internal rounds, and the like. This is especially true of angels and micro VCs. Both angels and micro VCs historically do not reserve much capital for follow-ons during the “good times”. The “spray and prey”, no follow-on reserves strategy only works when there is a steady supply of later stage capital to carry the portfolio companies forward. In these turbulent times, the later stage capital is experiencing its own liquidity crunch. As a result, many Seed and Series A investors are forced to choose between writing another check to an existing company or writing the company down in a few months. This reality leaves little money or appetite for new investments.

(c) Open to new investments but expecting a discount to pre-COVID-19 valuations. Complaining about sky rocketing valuations is every investor’s favorite pastime. Nevertheless, there is truth to the fact that valuations were likely overblown in the 2017 — Q1 2020 time frame. Some attribute this valuation inflation to ballooning late stage “unicorn” secondary markets. Others to a continuous oversupply of venture capital chasing an undersupply of quality deals. Regardless, investors confidence and willingness to absorb these historically high valuations showed first cracks in the fall of 2019, after a string of lackluster tech IPOs (hello, Uber) followed by the WeWork debacle. It then shattered to smithereens as the stock markets dived into a free fall the past two weeks. While it is not a representative sample by any means, in my work I am seeing investors push for 20% to 30% discounts to pre-COVID-19 valuations. The valuation discounts may become even steeper if the economy continues to deteriorate.

C. Expected Liquidity Crunch

Although there is always room for surprise, I expect the current situation to repeat in some aspects what happened to the tech industry in 2000 and 2008. There will be a liquidity crunch, where at least over the next six to twelve months the available pool of venture capital will decrease significantly. Lets examine what happened to the various investor types during the past downturns:

(a) Angels — are the first ones to stop writing checks to startups during a downturn. Majority of angels are high networth individuals who enjoy investing some of their discretionary income in startups. The key word here is “discretionary income”, which is very quickly dissipating for all of us, as almost any asset class falls in value.

The “super angels” — a minor subset of angels that invest professionally at scale, also stop investing during a downturn. Super angels pull the plug for different reasons. They typically redeploy capital away from startups to shorter term / higher profit opportunities available during recessionary times (for example, undervalued public companies or real estate investments). When faced with the possibility of picking up some real estate or public equities at a steep discount, a professional angel is unlikely to skip that bet in order to invest in a less liquid and riskier startup.

(b) Micro VCs — are smaller, often first time funds, and typically with less than $50M in AUM (assets under management). These funds have two unique challenges during a downturn. One is that by nature of their smaller size, during good times, they often prefer maximizing number of portfolio investments over keeping reserves for follow-ons. During tough times, same funds face a necessity to prop up the “stars” among their portfolio and quickly reallocate more capital to reserves. This leaves micro VCs with little to no capital for new deals.

Another challenge commonly faced by micro VCs during a downturn is defaulting LPs (limited partners). LPs are investors in the venture capital fund itself. Contrary to popular belief, a VC with $50M AUM does not actually have $50M in the bank. Instead, it draws anywhere from 10% to 25% of the capital commitments from its LPs each year during the active investment phase.

Also contrary to popular belief, LPs are not all created equal. They are as diverse as the funds themselves. It is highly unusual for first time funds to have large institutional LPs, such as endowments, funds of funds, foundations, and insurance companies. Micro VCs are mostly funded by high net worth individuals and family offices. Since these non-institutional LPs are more susceptible to market turbulence, they are more likely to delay or default on capital calls during a downturn. That leaves micro VCs on average with less capital then expected once the economy is in trouble.

(c) Thematic VCs — are funds of various sizes narrowly focused on a particular industry or theme. For example, a hardware fund, a life sciences fund, or a fund backing female entrepreneurs are all thematic VCs. If these funds are smaller, they can experience liquidity crunches of their own as described above. In general though, these thematic funds are more likely to continue investing during a downturn than generalist funds. That is assuming that their focus is not made obsolete by the prevailing market conditions. For example, over the next twelve months, I anticipate a drop of activity in travel and prop tech funds, vs. an increase of activity in life science and future of work funds.

(d) CVCs — are corporate venture capital funds. Some of them are structured as standalone funds with the parent corporation being the sole LP. Some are simply departments inside a corporation investing from the balance sheet. Typically CVCs focus on Series B and later rounds, so their activity does not have as much impact on the seed and Series A startups. Some CVCs have an earlier entry point but generally shy away from seed and Series A regardless during a downturn.

(e) Top Tier VCs — are the “Ivy Leagues” of VC world. There are many different opinions of who exactly is a top tier VC but they all share a few common characteristics. Majority have over $1B under management and are based in SF Bay Area. New York and Boston are second in concentration of top tier funds. Typically the top tier VCs are either pure generalists or operate a few thematic funds alongside a larger generalist fund. The good news is that top tier VCs by the sheer size of their funds cannot afford to sit on the side lines for too long. The bad news is that it becomes even more difficult to raise money from them during a downturn as the investment filters get much tighter. Another bad news is that historically top tier VCs focus on larger Series A and/or later stages, making them less relevant for your average seed or Series A startup.

D. Revisited Metrics

Prior years rewarded growth at all costs by sky rocketing private valuations and an active secondary market. In essence, an investor could realize a handsome profit by investing in a private company, holding the stock for a few years of cosmic growth, and selling the stock on the secondary market without the company ever having to turn a dime of profit. These times are clearly gone. As in past downturns, investors are a lot more conservative now and reward financial sustainability over hyper growth. As availability of down stream funding becomes less certain, investors prefer startups that can stretch runways, demonstrate sustainable growth, and reach break even with a modest amount of capital raised.

E. Game Plan for Success

In parting, I would like to share a game plan for successful fundraising during a down turn:

(a) Be realistic — about valuations, current market conditions, and timeline to close a round. It is better to be a pessimist than shut the doors once the money runs out.

(b) Be a survivor — now is not the time to trade money in the bank for possibility of the ideal round. Don’t make the mistake of letting go a good enough deal in pursuit of the ideal deal.

(c) Do your research — put together a target list of investors that are a fit for your company’s stage, geography, and sector. Do not waste precious time by trying to pitch everyone under the sun or focusing on investor types that are most likely to experience their liquidity crunches during a downturn.

(d) Lean on advisors — now more than ever, it is important to surround yourself with credible people who have networks and experience complementary to yours. A wartime CEO is very different from a peace time CEO and the two are often different people. If you are not a wartime CEO, you can still get yourself an advisor who has weathered a downturn or two.

Julian Zegelman is an early stage VC, tech investment banker, TCA member, and Father in Training (x2). Venture, Love and Sushi.

Reposted with permission from https://medium.com/@jzegelman/venture-in-the-time-of-pandemic